Here’s a situation that’s all too common in places like Delhi. You’ve got a solid business idea—a small workshop, maybe a catering service—and you know that ₹3-4 lakhs would be enough to get it off the ground. You go to a bank, feeling hopeful, but the conversation stops when they ask for property as security. For so many people, that’s a deal-breaker.

But what if it wasn’t? That’s exactly why the government started the Pradhan Mantri MUDRA Yojana (PMMY). It’s one of the most accessible and popular government loan schemes for small businesses, designed to fund the unfunded. The best part? No collateral required.

This guide will cut through the confusion. We’ll explain the different types of MUDRA loans, who qualifies, the latest interest rates for 2024, and give you a clear, step-by-step plan to apply for one online.

What is the MUDRA Loan? It’s Your Business’s First Step

MUDRA stands for Micro Units Development & Refinance Agency Ltd. Think of it not as a direct bank, but as a supportive partner to banks. MUDRA provides refinance to banks and NBFCs, encouraging them to lend to micro and small businesses without the fear of high risk.

In simple terms, the government backs the lender, so the lender can back you.

The core mission is to empower small income-generating activities across sectors—from auto repair shops and beauty parlors to local artisans and tech-enabled service providers.

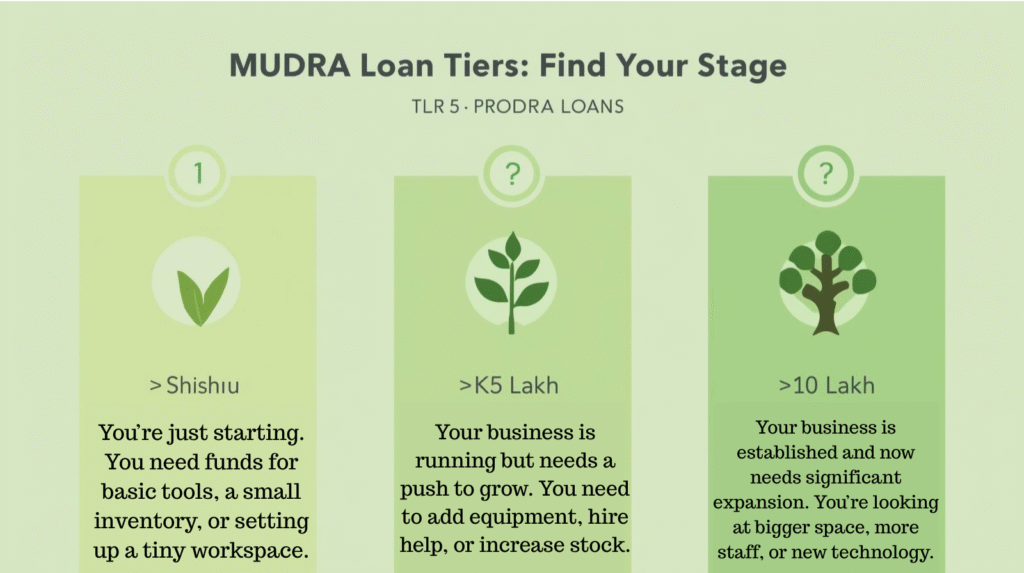

The Three Categories: Shishu, Kishore, and Tarun

our business’s growth stage determines the loan amount you can apply for.

Your business’s stage determines how much you can borrow. MUDRA loans are beautifully categorized into three stages, named after the phases of growth.

Category

Loan Amount

Who It’s For

Ideal For

Shishu (The Infant Stage)

Up to ₹50,000

You’re just starting. You need funds for basic tools, a small inventory, or setting up a tiny workspace.

Buying a sewing machine, a mechanic’s toolset, a small juice-making unit.

Kishore (The Adolescent Stage)

₹50,001 to ₹5,00,000

Your business is running but needs a push to grow. You need to add equipment, hire help, or increase stock.

Adding a second machine to your workshop, buying a fridge for your catering business, opening a small kiosk.

Tarun (The Young Stage)

₹5,00,001 to ₹10,00,000

Your business is established and now needs significant expansion. You’re looking at bigger space, more staff, or new technology.

Expanding your retail shop, buying a small delivery vehicle, setting up a computerised system.

The most powerful feature? Loans under ₹10 lakh are provided without any collateral. This is the game-changer that has made crores of rupees accessible to small entrepreneurs.

Who is Eligible for a MUDRA Loan? (The 2024 Checklist)

The eligibility criteria are broad by design, to include as many small businesses as possible.

✅ Type of Business: Non-corporate, non-farm small/micro enterprises. This covers a vast range: from street vendors and shopkeepers to small industries and service providers.

✅ Business Age: Both new and existing businesses are eligible. There is no strict “age of business” limit.

✅ Loan Purpose: The loan must be for income-generating business activities. It cannot be for personal use like a wedding or a car loan.

✅ Residency: The applicant must be an Indian citizen.

✅ Credit Score: While a good CIBIL score helps, many banks offer these loans to applicants with no prior credit history, based on the business proposal.

Who is it NOT for? Large businesses, corporate entities, agricultural farming (though agro-processing units are eligible), and activities like retail trading of illegal goods.

MUDRA Loan Interest Rates 2024: What to Expect

That’s the big question, and the answer is: it depends. There’s no single, fixed interest rate for MUDRA loans.

The rate you get is actually set by the bank or lender you go to. Because it’s a government-backed plan, the rates are usually much better than a normal business loan. Right now, you can expect something in the range of 8.5% to 15% per year.

As a general rule here in Delhi, government banks like SBI or PNB will likely give you a rate on the lower end. Private banks might be a bit higher, but they could process your application faster.

A bit of advice: Don’t just accept the first offer. It pays to shop around and ask a few different banks what rate they can give you.

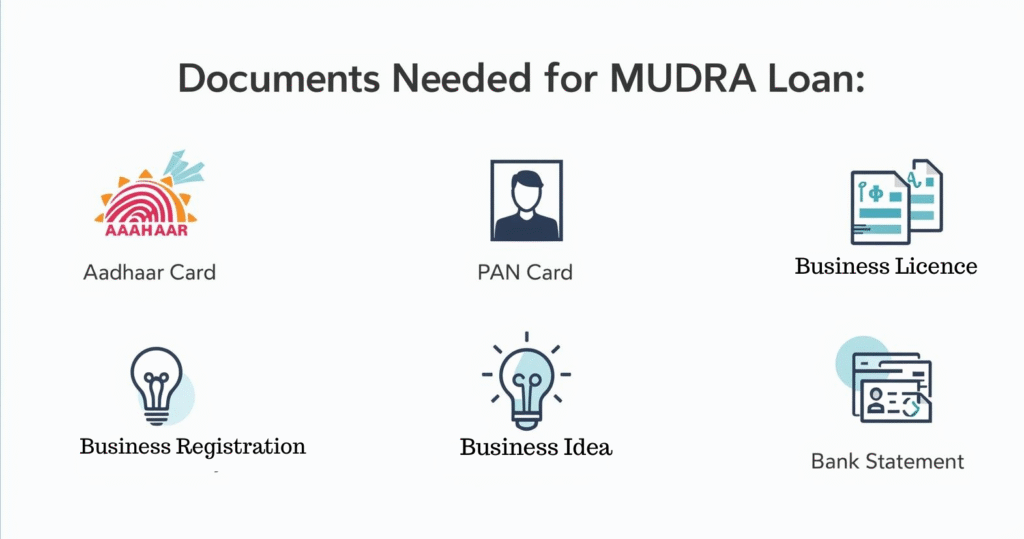

Documents Required for MUDRA Loan Application

Banks can be particular, but here’s what they almost always ask for. Have these ready to speed things up.

Proof of who you are and where you live: Your Aadhaar and PAN card are best.

Some passport-sized photos.

Proof your business is official (if it’s already running): Things like your GST registration or trade license.

A basic, one-page business plan: This is crucial if you’re new. Just outline your idea, your costs, and your repayment plan.

Your business’s bank history (if applicable): A 6-month statement will do.

Being prepared with the right paperwork speeds up the application process.

How to Apply for a MUDRA Loan: Online & Offline Steps

Contrary to popular belief, there is no single “Apply Now” button on a national website. The application is channeled through banks.

Step 1: Choose Your Lender (Bank/NBFC)

Approach any bank (public, private, regional rural) or NBFC that is a member of the MUDRA scheme. Almost all major banks are. You can start with the bank where you already have an account.

Step 2: Prepare Your Business Proposal

Be clear about how much you need (Shishu, Kishore, or Tarun) and exactly what you will use the money for. The bank manager will want to hear a confident, well-thought-out plan.

Step 3: Submit the Application & Documents

Fill out the bank’s specific application form for a business loan or MUDRA loan. Submit it along with your KYC and business documents.

Step 4: Bank’s Verification Process

The bank will verify your documents, may visit your business premises (if existing), and assess your creditworthiness.

Step 5: Loan Disbursement

Once your loan is approved, the bank will transfer the money directly into your account. Be prepared to wait a bit—the whole thing usually takes anywhere from one to a few weeks.

As for applying online, you can start the process on some bank websites, like SBI’s. But you’ll likely still need to visit the branch in person to submit documents and finalize everything.

MUDRA Loan vs. Other Schemes: Which is Right for You?

Wondering how this compares to other options?

vs. CGTMSE: The CGTMSE scheme also offers collateral-free loans but is focused more on larger MSMEs and can cover loans up to ₹2 Crore. MUDRA is for smaller, micro-units.

vs. Business Credit Card: A credit card offers revolving credit but at a much higher interest rate. A MUDRA loan is a term loan with a fixed, lower EMI.

vs. Personal Loan: A personal loan can be used for anything but has a higher interest rate and shorter repayment tenure. A MUDRA loan is cheaper and has a longer tenure because it’s for business growth.

Frequently Asked Questions (FAQ)

Q1: What is the maximum repayment tenure for a MUDRA loan? A: The maximum repayment period can be up to 5 years (60 months), depending on the loan amount and the bank’s policy.

Q2: Is there a subsidy on the interest rate? A: No, there is no direct interest subsidy from the government. You pay the interest rate charged by the bank. However, the rates are concessional.

Q3: Can I get a second MUDRA loan? A: Yes, you can apply for another MUDRA loan, either for expanding your existing business or for a new venture. The total outstanding amount across all MUDRA loans should not exceed the limit of ₹10 Lakh.

Q4: What if I default on the loan? A: Defaulting will negatively impact your credit score (CIBIL) and make it very difficult to get any loan in the future. The bank will initiate recovery proceedings. It is crucial to only borrow what you can confidently repay.

Q5: Can I prepay the loan? Is there a prepayment penalty? A: Most banks allow prepayment of MUDRA loans without any penalty. However, it’s always best to confirm this with your specific lender before signing the agreement.

The PM MUDRA Yojana is more than just a loan; it’s a belief in the dreams of India’s smallest entrepreneurs. It acknowledges that a small push at the right time can create not just a sustainable business, but also generate employment and strengthen the local economy.

If your need is larger or your business is more formalized, also explore the options under the CGTMSE scheme for collateral-free loans up to ₹2 Crore.

{kind=link}